{kind=link}

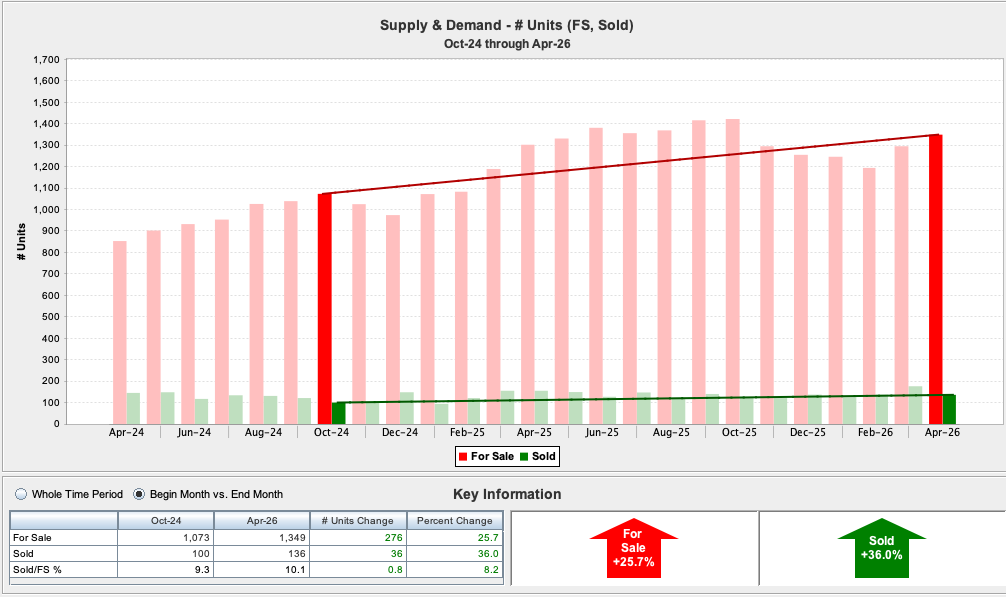

$1M–$3M: The Foundation Remains Strong

The $1M–$3M segment continues to anchor the market, accounting for the majority of activity. 1,349 homes available. 176 pending sales. 136 closed sales. Pending sales are up nearly 16% year-over-year, pointing to steady demand. At the same time, median pricing has remained essentially flat at $1.33M, reinforcing that this segment is experiencing stability over appreciation. Well-positioned homes—those priced correctly and presented at a high level—are still moving. Overpriced or dated inventory is sitting longer.

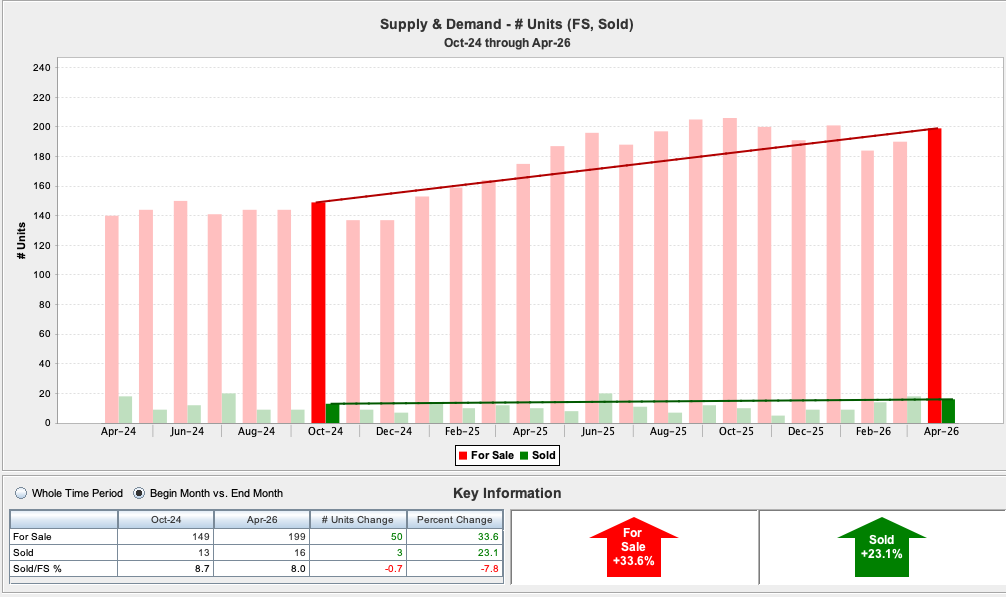

$3M–$5M: Activity Surges, Pricing Adjusts

This segment saw one of the most notable shifts in April. Pending sales increased 33% year-over-year. Closed sales jumped 60%. Median price declined to $3.3M (down ~13%). The takeaway: buyers have returned, but with leverage. Increased inventory has created more opportunity, and buyers are capitalizing—often negotiating below prior peak pricing. This is a segment where strategy and positioning are critical.

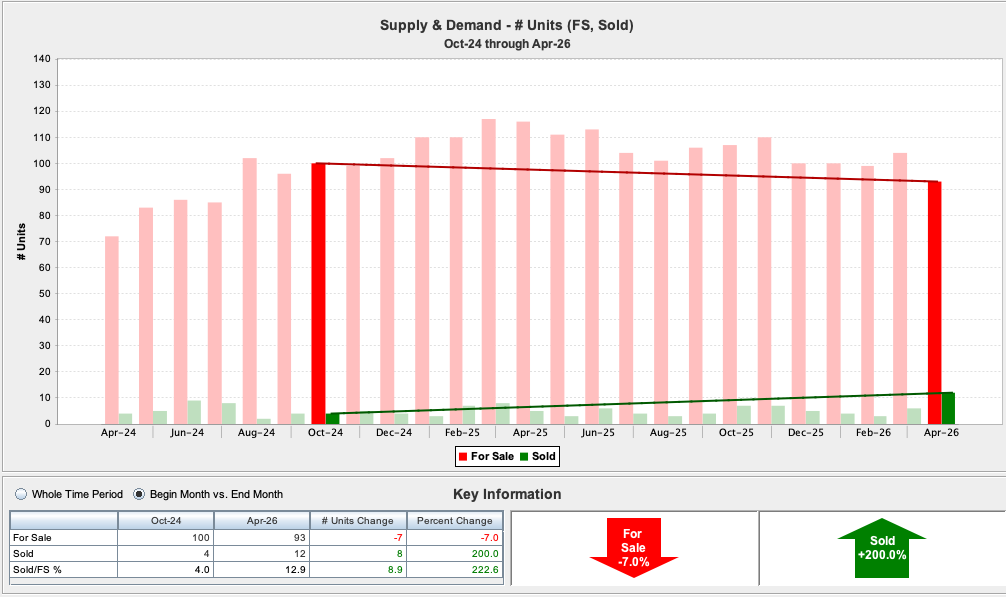

$5M–$10M: The Standout Performer

The $5M–$10M market was April’s strongest story. Inventory decreased nearly 20% year-over-year. Sales more than doubled (from 5 to 12). Median price rose to $6.6M (up ~14%). This indicates a clear shift: high-net-worth buyers are re-engaging at the upper end, particularly for turnkey, high-quality properties. As seen nationally, ultra-affluent buyers are less impacted by financing conditions and more driven by lifestyle, privacy, and long-term value—fueling strength in this tier.

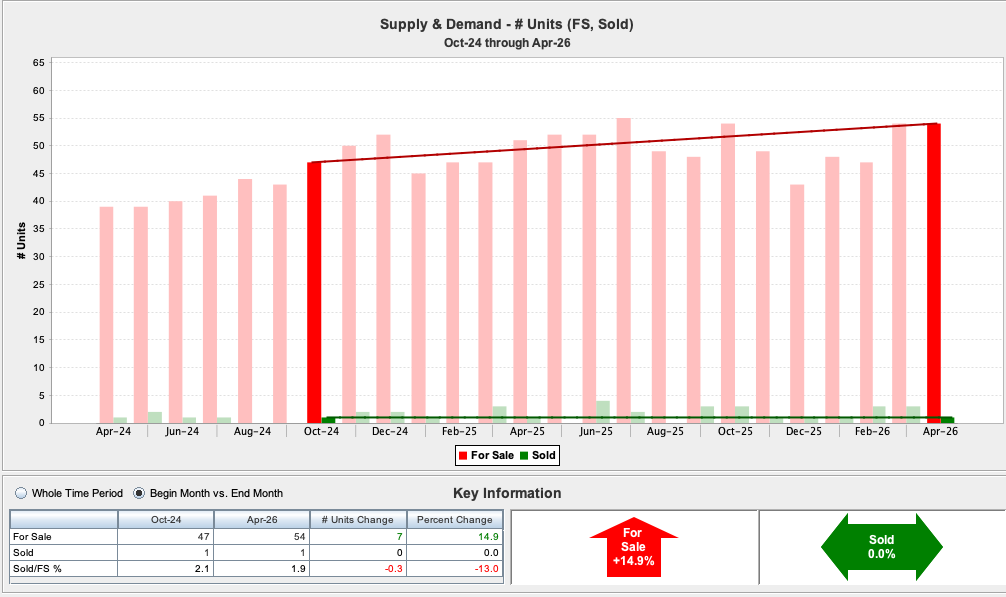

$10M+: A Selective, Deal-Driven Market

At the very top of the market, activity remains limited but meaningful. 54 homes available. 1 pending sale. 1 closed sale. Median price: $10.5M. This segment continues to operate on a case-by-case basis, where each transaction depends heavily on the uniqueness of the property, pricing strategy, and access to the right buyer.

Overall Market Insight

At a Glance: April vs. Last Year ($1M+) Active Listings: 1,695 ⬆️ (+3.1%) / Pending Sales: ⬆️ +18.1% / Closed Sales: ⬇️ -3.5% = Key Takeaway: Buyer activity is up—but deals are taking longer to close. This is a more thoughtful, selective market.

Final Takeaway

April’s data reinforces a clear narrative: Inventory is rising—but not evenly across all price points Buyer activity is improving, particularly above $3M Pricing is stabilizing, with negotiation more common in mid-luxury tiers. The $5M+ market is regaining momentum. We are no longer in a market defined by urgency. Instead, we’re in a market defined by precision. For sellers, success requires accurate pricing, strong presentation, and strategic exposure. For buyers, this is a window of opportunity and choice not seen in recent years.